Jeroen Kakebeeke Sr.Investment Risk Manager at PGGM Informs on A Perfect Storm

Jeroen Kakebeeke is the Senior Investment Risk Manager at PGGM Investments. In this white paper he reports on the Corona Pandemic, the Economy and the Financial Markets as of March 25, 2020.

Introduction

End of January I recommended strongly to sell equities because of the Corona crisis. When to come back in the stock market? This is my second investment letter with updated insights.

Financial Markets

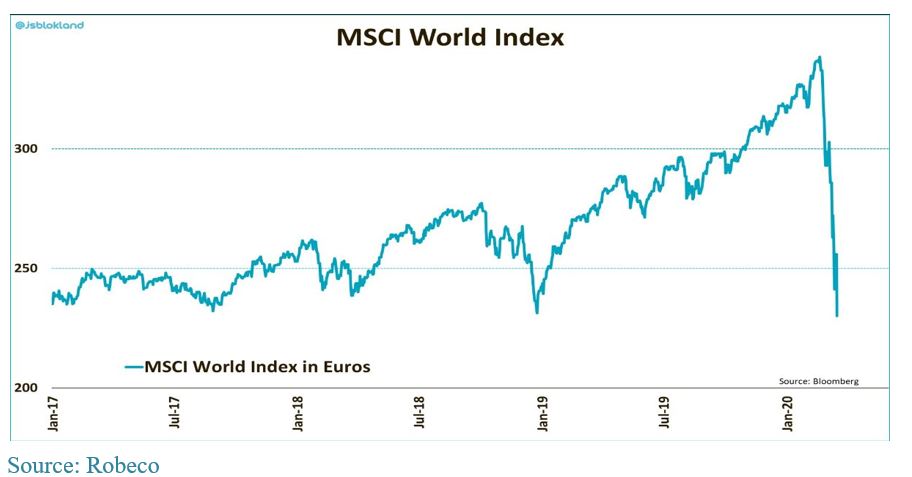

In four weeks time the stocks markets lost about 33% in value and volatility quadrupled!

We experienced a major shift in sentiment, from greed to fear, because:

- Nobody knows how long the Corona pandemic will last or how severe it will be.

- At the start of 2020, stocks were trading at historically high valuations.

- The health crisis will trigger an overdue recession in the next months.

- The financial shock causes negative Wealth Effect and Loss of Confidence.

During the Corona crisis the services sector has had a clear and direct hit: airlines, transport, tourism, hotels, restaurants have seen their revenues more than half (and profits evaporate). A second order effect is visible in discretionary goods, advertising, temping, automobiles, airplanes, steel, banks (non-performing loans), and insurance (increased cost of Corona patients and deaths). Also chemical, pharma, tech, and industrial companies are hurt by the supply disruption, and suffer from soft demand as well. Beneficiaries are supermarkets, selective online retailers, and telecom.

In comparison to the 2008/09 crisis banks are much better capitalized, this sector is punished too harsh in my opinion. In comparison with the 2001 bubble, tech is currently not more overvalued than the rest of the market. I understand why the tech-monopolists are expensive, and their business is scaleable, so they can adapt to a low growth environment. If those last two recessions are an indicator, we have about a -50% drop for the S&P 500.

Another way to estimate stock market losses is adding up three adjustments:

-15% from overvaluation (on a diversified set of valuation ratios);

-15% real economic damage (on average one year no profit or dividend in the DCF models); and

-15% to undervaluation: fear, margin sells, insurers and pension funds face obligatory (regulatory) selling, leveraged companies have to sell assets.

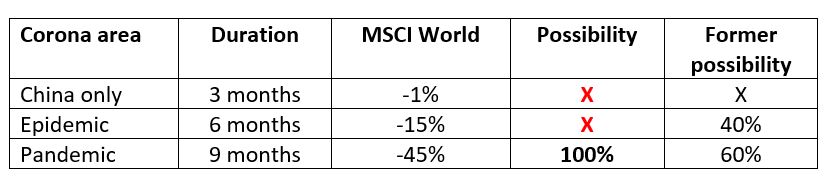

To conclude, 45% to 50% downside is warranted. And I projected it would come in four waves, in accordance with the epicenter of the pandemic: from China, via the Pacific and Europe to the US.

For the global equity scenarios, only one option remains in my opinion:

Frankly, I am surprised by the speed of the equity crash. And who not? These Corona crashes are of historical magnitude! Three one-day losses rank in the all time top 10, amidst the worst days of the 1987 and 2008 bear markets. Often those large downward moves are followed the next day by a Dead cat bounce. Investors who neglect the medium term are buying the dips. Or day traders and speculators feel the Fear Of Missing Out, and they buy to follow the herd in hopes for higher.

Even when all equities seem cheap, I am reluctant to buy the dips yet. Reported company results over 2019 and estimates over 2020 are worthless. During the Corona crisis every estimate will be downgraded. The pandemic is accelerating at the expense of GDP, sales, profits, and some dividends. We know the scale of downgrades only when the crisis is over. Currently the outlook is worsening almost by the day. I expect a last 10% to 15% downside for equities in the fourth wave, when the virus is taking over the US.

Central Banks and governments took adequate actions to prevent a further economic fall out of the Corona pandemic. With the US Treasury rate at zero and negative interest rates by the ECB, safe government bonds have reached their most expensive levels ever. Expect negative return for coming years. How to proceed in the investment portfolio then?

Risk management helps to get grip on emotions in turbulent times. Scenario analysis helps in understanding the current environment and the next possible developments. Try to follow a defined scenario-path, with limits on exposures and be ready to change plans when the facts differ from expectations. Risk reduction is done via diversification; across geographic markets, sectors, duration, and asset types, including having sufficient liquidity.

I know it is impossible to time the bottom of the market. During this Corona panic all assets are sold – including gold, bitcoins, and safe credits – there seems no bottom. Cheap assets can become even cheaper, volatility remains high. Currently, risk-return seems asymmetric and attractive, in that long term upside is larger than near term downside. I see some sector rotation and individual stocks reacting on specific company news. As if panic is replaced by fundamental analysis. Step (back) in the market incrementally, with several small orders.

For a sustained recovery in equity markets, we need signals that the virus outbreak is peaking, just in the case of China. Wait for the light at the end of the tunnel! Jeroen Blokland (Robeco) noted: Keep in mind however, that markets will try to anticipate this inflection point well in advance.

We will overcome the market crash. I expect this summer to lay the seeds for a beautiful equity portfolio. And leave it grow for a decade, till the next perfect storm.

To see the full white paper with Jeroen's insights on the economy and recession, and his assessment on when we will overcome the pandemic click here or download as a PDF below.

drs Jeroen Kakebeeke RBA is an Advisory Board member of Institutional Investor. His profession is Investment Risk Manager for a large pension fund. The views expressed in this paper are his own. To discuss the content of this article and further engage with him, comment below.