Jeroen Kakebeeke Sr. Investment Risk Manager at PGGM Informs on Waves

Jeroen Kakebeeke is the Senior Investment Risk Manager at PGGM Investments. In this white paper he reports on the Corona Pandemic, the Global Economy and the Financial Markets as of July 30, 2020.

Introduction

At the end of January I strongly recommended to sell equities because of the Corona outbreak. Financial markets completely overlooked consequences for the economy and companies. In my second investment letter of March I gave a roadmap to rebuild the investment portfolio, and in May I advised to underweight Government Bonds and Emerging Market Equities. You can see both papers here and here. In this fourth letter I share the latest ideas about global risks and returns.

Corona

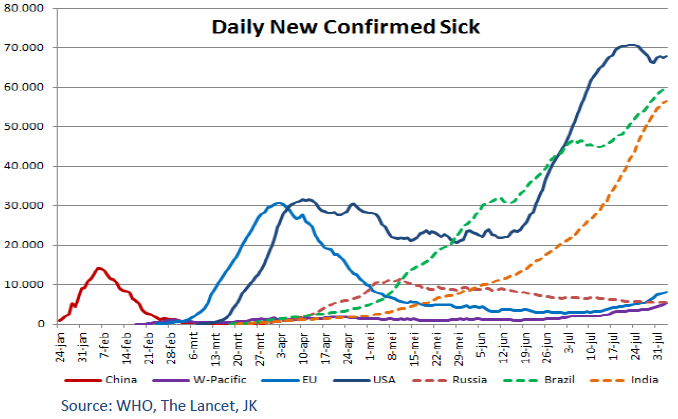

It is necessary to understand the Corona pandemic to make any forward looking statements on the economy or financial markets. Although we know the numbers of infected and dead are incomplete (underreported), they give direction. Globally, the pandemic is not under control! Some societies have adapted, especially in the West-Pacific region where infections remain low. In Europe, infections remain smoldering, flaring in tandem with opening of the economy. Some fact denying populist presidents gave freedom: to the people, to the economy and to Corona. Now Brazil, Russia, India, Mexico, South-Africa, and the US are at the same side as most Emerging Markets, where governments don’t have the means to fight the virus.

Unfortunately, waves of new infections are visible on all continents. Also rolling within a country, in the US from New York to the South-West, and back again. The deaths are a tragedy, the confirmed sick are a bellwether for economic damage. In Developed Markets there is no trade-off between controlling the spread of the virus and resuming business or public life. Physical distancing will be the norm for as long as a vaccine is unavailable. Only wealthy governments like the US, Japan, and European countries have reached deals to secure in 2021 hundreds of millions of doses of a vaccine-yet-to-be-proven.

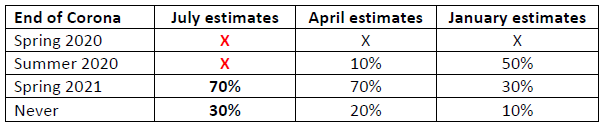

The expected duration of the pandemic has changed. The stealthy virus makes eradication near-impossible, medical experts say. Also the short half-life of antibodies explains why some got sick for a second time, and makes it scary to realize that herd immunity will probably never be realized (King’s College London, July 2020). Corona still has many unknowns: how lung and heart tissue is damaged/repaired, what is the relation to fatigue, other impacts of the body, and how bad will winter season be?

Economy

The imposed lockdowns have sent a shock wave through the global economy. The fall in GDP is larger than at the time of the Great Depression. Politicians and Central Banks have taken bold counter measures, where the taboo has been broken to enlarge government debt beyond old limits. The money is for direct support to unemployed and companies in need. Central Banks print money and monetize debt by another wave of asset purchase programs.

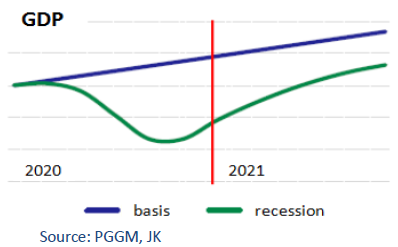

China was first to reopen their economy, and the only country to post a positive GDP in 2Q. But the hoped V-shape recovery is absent. It takes longer to restart factories, global trade stands still, people fear contagion and go voluntarily in lockdown. Consumers spend less money because of income uncertainties and the need to rebuild a financial buffer, companies face an output gap, governments miss tax proceeds. Economists call it the multiplier/second order effect. IMF estimates a cumulative loss of USD 9 trillion GDP over 2020 and 2021, while global GDP is $90 trillion. In the graph the area between the blue (basis) and green (recession) line. The crises set GDP levels and prosperity more than one year back in time.

In June, IMF updated its World Economic Outlook 2020. In two months’ time GDP estimates deteriorated by 2% points, since the Corona Pandemic was worse than expected.

Between countries we see a remarkable small difference in GDP trajectory. China being the exception, the only country with growth. The US is disappointing. Trump could not suppress the virus, that policy failure is a drag on the economy. The US needs again a trustworthy and intelligent president. Unfortunately, autocrat Trump has said more than 18,000 false or misleading things in his 1,170 days in office. An average of 15 incorrect claims every single day since he has been president, according to The Washington Post's Fact-Checker blog.

Between sectors we see a big difference in revenues. Energy, Financials, Industrials, Real Estate, Beverage, Consumer Discretionary and need on average two till three years to bring profits back to pre-Corona levels. IT Hardware, Chemicals, Food, Telecom, Utilities have stable results. Internet and Health Care clearly benefited. In Europe, Health Care has the largest sector weight and six stocks are in the top 10 by market capitalization.

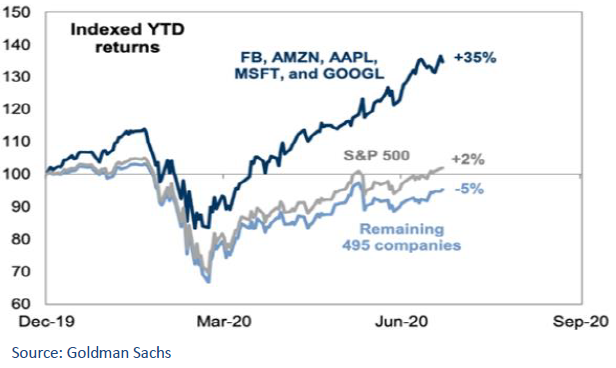

Internet stocks are in the sweet spot. Corona is a catalyst in the trend towards digitalization: on-line shopping, working/learning from home, gaming, movies, software, Internet of Things, artificial intelligence, machine learning, cloud services. The acronym FAMAG stands for Facebook, Apple, Microsoft, Amazon and Google. These five US Growth stocks dominate the S&P index with a combined 25% share. Lower interest rates elevated their PE-ratios. These cash rich, global monopolystic companies beat repeatedly revenue and profit estimates. The recent House Judiciary Subcommittee Hearing seems not to change that.

See in a graph the outperformance of Big Tech. The remaining 495 companies are a more meaningful gauge of how the outlook for the US economy has developed.

Financial Markets

Safe government bonds have reached their most expensive levels ever, with US interest rates near zero and negative interest rates by the ECB. In three months’ time the risk free rate fell circa 1% point. Fixed income investments do not deliver a positive return without risk. Expect negative performance for coming years, safe government bonds are less attractive.

Standard & Poor’s reported so far 55 defaults on corporate bonds in the US. Entertainment, energy and retail were the obvious sectors with most casualties. Defaults are a lagging indicator, the worst has still to come. High Yield defaults are expected to rise to 11% in the US and 9% in Europe. Credit spreads have adapted. The total stock of deferred loans held by banks is accumulating into hundreds of billions. This emphasizes the wording of Central Bankers: during the GFC banks were part of the cause; this time banks are part of the solution.

Developed Market Equity quickly recovered from the Corona led shock wave. It was directly linked to government support for the economy, which prevented a meltdown – and indirectly to Central Bank intervention to lower risk free interest rates. This makes corporate debt cheaper, and more importantly, makes equity more expensive in valuations.

Investors use Discounted Cash Flow (DCF) calculations in pursuit of the intrinsic value of securities. This is a strong theoretical and practical model, ranging from simple to very complex. Pre- and post-Corona, a DCF calculates 25% higher valuation on 1% point lower risk-free rate, ceteris paribus. One could argue that the US risk-free interest rate is artificial low, caused by Central Bank intervention and not determined by a free market.

Is it fair to calculate with such a low rate then? Yes, currently it is the observed and traded interest rate. The reality is that Central Banks will keep rates lower for longer. It is the new normal, it is part of secular stagnation. Central Banks will help their hefty indebted US and European governments with low risk free interest rates. When inflation rises debt becomes more sustainable, so inflation will not be suppressed immediately.

A simple DCF sets the Price/Earnings ratio equal to the Free Cash Flow divided by WACC-adjusted-for-eternal-growth. In formula: FCF/(WACC-G). Most realistic inputs are 5% WACC and 1% growth, but 6% WACC and 2% growth is fine, too. Both result in a PE-ratio of 25 for the general equity market post Corona, coming from 20 pre-Corona.

FactSet EPS estimates are in a downward trajectory over the current crisis year. Next year is best to set a target for US S&P 500, with a forward PE of 24. The aggregated analysts estimate is $150. With both EPS and PE-ratio higher, my target rises from 3.100 to 3.600.

US equity is an attractive asset class with decent upside potential, based on these calculations. Asian and European equity offers comparable expected returns. The US has often higher valuation ratios because the country enjoys multiple competitive advantages: a big home market, demographic growth, educated workforce, technological innovation, flexible hire/fire policy, enterprise friendly financial system, sufficient infrastructure, global reach, transparent legal regulation and protection, USD as world reserve currency, and military protection.

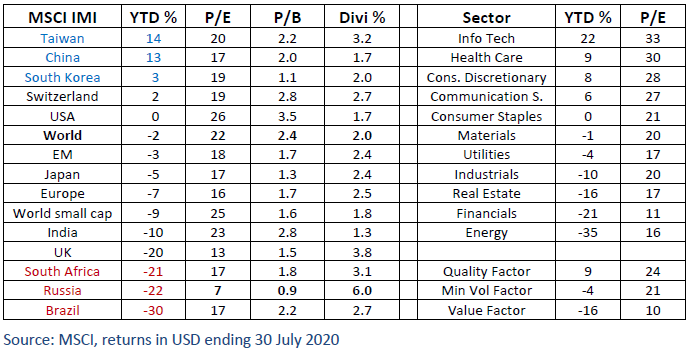

In the performance attribution of MSCI country indices, Corona is a clear and present danger:

- the three-highest ranking countries have the best control over the epidemic (East Asia);

- the five lowest ranking countries have the worst control over the epidemic;

- the four lowest ranking countries saw 15% currency depreciation (low trust);

- cheapest country (low trust) Russia has 55% allocation to Energy;

- highest ranking Western country Switzerland has 40% allocation to Health Care;

- UK equity market has become a Value play. Due to worsening virus outbreak and the upcoming Brexit, it is understandable the country is out of favor. But these low valuations seem overdone. For the index as a whole, including domestic and international companies.

Emerging Markets are a broad diversified bucket of countries. EM occupies both the top 3 as well as the bottom 3 ranking. Differences come mainly from: culture, leadership, debt levels, dependency on tourism or production, oil imports versus exports. Some Emerging Markets cannot impose a lockdown. Many dayworkers in the informal sector have not the luxury to work from home. And a day not working means often a day without income, possibly even without food. Physical distancing and hygiene upkeep is impossible in crowded slums. When Corona stays longer, and with less financial cushion, the outlook is grim.

Conclusion

Short term, the Corona pandemic remains in the headlines. The virus has a longer duration, and economic consequences are not precisely known, thus weighing on financial markets. Full-scale lockdowns seems unlikely, the economy will muddle through. Most assets have adapted and are fairly priced. Equities are attractive, albeit with higher volatility. The Corona crisis aggravates other major economic risks: Brexit, US-China Cold War, oil war, debt mountain, and climate crisis.

drs Jeroen Kakebeeke RBA is an Advisory Board member of Institutional Investor working as Investment Risk Manager for a large pension fund. The views expressed in this paper are his own. The author thanks Kiemthin Tjong Tjin Joe for his valuable ideas.To discuss the content of this article and further engage with him, comment below.